Q4 2017: Maturing Global Economy Broadens

The US economy posted solid growth in 2017; corporate profits rose and unemployment declined toward 4%. Stock market valuations are at levels consistent with the late stages of previous market tops. However, every market cycle is unique, and this one may not yet be over. It has been said that markets die on euphoria. However, optimism was probably the better word to characterize the 2016-17 time frame. A euphoric condition feels a lot more like a Gatsby party, with unexpected people boasting of huge profits in assets they don’t understand and where prudent topics like risk and uncertainty are met with rolling eyes. If we are right about the stages of the human condition, then markets are moving from optimism to euphoria as we begin 2018. But no two cycles have ever been the same and nothing beats a good plan. For us, that means having a reasoned investment premise, based on real evidence, properly sized within risk budgets and having a sound exit strategy.

As we enter 2018, we are highlighting these thematic inputs when making investment allocation decisions:

Inflation:

- Building upward pressure;

- Nearing full employment in the U.S.;

- Willingness (or even a need) by central bankers to let inflation rise.

Government:

- Easing of regulatory standards;

- Tax code changes friendly to corporations.

Optimism and Euphoria:

- A real global growth cycle;

- GDP in the US is growing and activity is broadening;

- Easy money conditions;

- Strong capital flows into growth assets.

Growing Inflationary Pressures

Late stage bull markets often experience building inflationary pressures. Workforces become fully employed, demand outstrips supplies and raw materials prices increase. A devaluation or depreciation in the local currency can increase import costs and cause “cost-push” inflation. In 2017, several commodities (oil, copper, lumber) rose in price, and the dollar declined. In 2018 and beyond, the new tax cuts will cause larger deficits and force greater US Treasury borrowing, which will put downward pressure on the US dollar. The Euro is likely to gain strength relative to the dollar as the EU winds down its current QE program later in the year. Central bankers want inflation, and may be willing (but will never admit) to be behind the curve a bit. Inflation is essential to debtor economies.

All this takes time to build. Inflation will probably not become a problem overnight. But we are highlighting inflation as the primary consideration for US investors in 2018-19; not because it is a certainty, but because IF inflation does rise, and increase in upward velocity, it could be the most damaging of any observable scenarios.

The elevated risk of rising inflation, coupled with a pro-business government and investor sentiment moving from optimistic to euphoric, influence investment allocation decisions in new ways. Our allocation decisions are built from a top down perspective. We start with the factor that has the most impact on return outcomes and move on to those that also attribute to portfolio results in a descending pattern. Risk budget (derived from the planning and investment policy process) is most important as it determines the degree to which capital is placed “at risk” and seeking positive returns. Asset class allocation decisions are less important than risk budget allocations but more important than investment holding decisions.

Here is a brief summary of factors influencing our allocation decisions:

- The Fed will raise rates several times

- Commodity prices should continue to rise

- The dollar will decline (especially in the 2nd half of 2018)

- Leadership in US stocks (and sectors) will rotate

- Emerging market stocks are undervalued relative to developed countries

Primary risk considerations:

- Inflationary pressures

- High valuations in U.S. growth assets

Snapshot of anticipate 2018 actions:

Risk Budget

Maintain at 100% of current levels

Risk Allocation

- Rotation within US equities (to benefit from tax changes, regulatory changes and inflationary pressures)

- Reduce US equity exposure

- Increase Emerging Market exposure

- Reduce long dated bonds

- Increase credit quality of fixed income

- Increase commodity exposure

The net effect of these actions should reduce exposure to primary risks – rising rates, inflation and high US equity valuations – but should also maintain full risk budgets. This should improve forward return potential by allocating into lower multiple equity assets.

We believe that buying emerging market equities, and to a lesser extent, international developed equities provides diversification, increases our forward return expectations and allocates capital from high priced assets into both quality and value assets. Investing in emerging markets does not mean buying speculative ventures in fragile countries. Simply comparing the large-cap stocks in established foreign countries to US counterparts shows significant discrepancies between markets. US large-cap stocks are trading at 24x earnings and are priced at 3x book value. By comparison, stocks of similar foreign companies trading outside the US are at 12x earnings and 1.2x book value. In addition, there are three other considerations that make emerging market investments timely:

- Emerging market countries have larger portions of their economies that benefit from rising inflation and commodity prices;

- The synchronized global economic expansion is a greater tailwind for emerging economies;

- US dollar weakness would compound the gains in EM stock allocations.

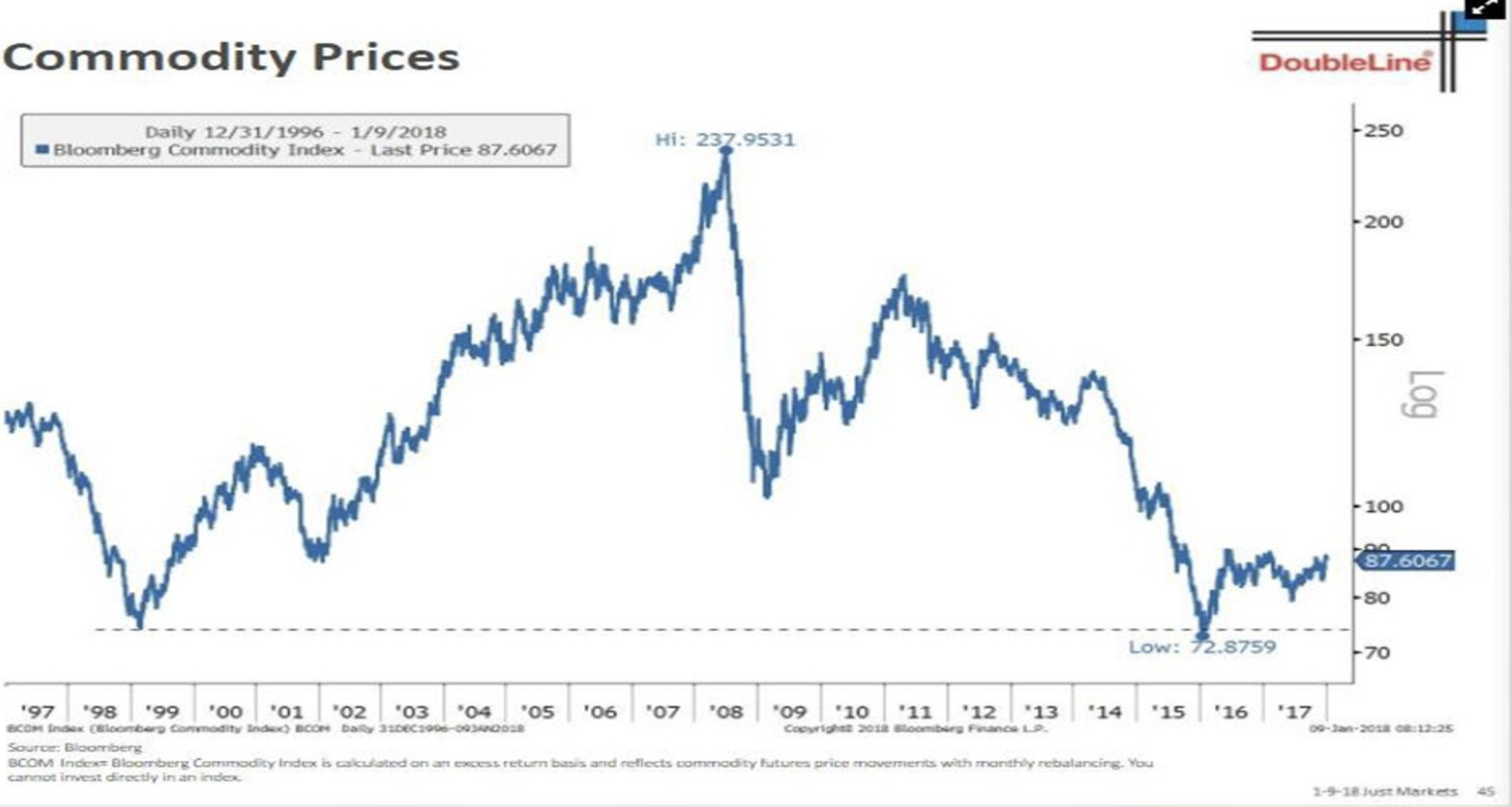

We also believe that a moderate increase to commodity exposure through US equity sector over weights and direct commodity basket ownership could improve return outcomes in the next several years as global economic activity expansion and full employment push supply constraints. We see this as a satellite investment allocation that is part of the normal risk budget, with low correlation attributes and a good risk/reward contributor to portfolios. Commodity prices almost always rise in the late stages of an economic expansion, and as the chart below shows, commodity prices are still very low on a historic basis:

It is worth pointing out that this commentary update is focused on our 2018 actions. And much of what we see in early 2018 is continued support for growth assets. However, it is important to note that risks are building in most asset classes, and that a reset or mean reversion event would have a fairly sizable downside for portfolios. The current environment is not a place for short-term money, and we strongly recommend that any funds needed in the next several years be placed into capital preservation and safety. Quantifying risk and moving the necessary amount

Comments are closed.